Deciphering Monetary Policy as a Means to Beat the Market

(Originally published October 2012 by Adagio Group)

Monetary policy and its effect on the markets can often seem as an impossibly complex, if not opaque dynamic. The market obviously responds, and most often in a seemingly positive manner, to the actions taken by the Federal Reserve System and statements by its chairman, Ben Bernanke… but how and why, and what are the less obvious effects of a centralized monetary system?

Money is a market chosen commodity that serves as a recognizable, divisible and portable medium of exchange and store of value. Historically gold and silver have served this function. The term “dollar” as cited in the U.S. Constitution (Article 1, Section 9, Clause 1 and the 7th Amendment) and specifically defined under the Coinage Act of 1792 “to contain three hundred and seventy-one grains and four sixteenth parts of a grain of pure, or four hundred and sixteen grains of standard silver” is a reference to the Spanish milled dollar, a silver coin. The authors of the U.S. Constitution had learned the dangers of issuing unchecked fiat currency first-hand when the Continental Congress issued its own paper currency, the infamous Continental, as allowed under the Articles of Confederation… the result was economic chaos. In one of the only instances in world history where the politicians who created an egregious problem recognized their mistake and corrected it, the Continental Congress later repaired to Philadelphia drafting the U.S. Constitution explicitly maintaining gold and silver as tender in payment of debts (Article 1, Section 10, Clause 1). Centuries of pressures to fund war and appease the banking cartel have ultimately reversed this act of wisdom.[1]

THE FEDERAL RESERVE & “SYSTEMICALLY IMPORTANT BANKS”

The Federal Reserve System (“the Fed”) is the central banking system of the United States. The Fed is said to be independent within government in that "its monetary policy decisions do not have to be approved by the President or anyone else in the executive or legislative branches of government." The Fed has both private and public aspects; there are 12 Federal Reserve Banks that are owned by their respective member banks while the Board of Governors, which is a federal agency in and of itself, is appointed by the President of the United States.[2] It is worth noting that other than the 6% dividend paid to the Fed’s shareholders (i.e. its member banks), the profits of the Fed are returned to the U.S. Treasury, and member banks do not exercise the proprietary control traditionally associated with the concept of ownership beyond the statutory dividend.[3] Member banks do, however, elect six of the nine directors for their regional Federal Reserve Bank board; each Federal Reserve Bank board of directors appoints its bank president. Ownership in the twelve Federal Reserve Banks is not public record, but national banks must be members while state chartered banks may become members by meeting certain requirements.

The Fed was established via the Federal Reserve Act, which was passed by Congress and signed into law by President Woodrow Wilson on December 23, 1913. The passage of this act granted the Fed exclusive right to issue the U.S. national currency, Federal Reserve Notes, at the discretion of its Board of Governors with the five regional Fed Bank presidents making up the Federal Open Market Committee (“FOMC”). Federal Reserve Notes, or “dollars”, were redeemable in gold until the Emergency Banking Act of 1933 removed that obligation. Federal Reserve Notes from that point on were redeemable only for other Federal Reserve Notes (effectively making change). On April 5, 1933 President Franklin Roosevelt signed Executive Order 6102 criminalizing the possession of monetary gold in quantities exceeding $100. All U.S. citizens and businesses were required to deliver their gold to the Fed in exchange for $20.67 per once. The price of gold was then raised by the Treasury to $35 per ounce. Although citizens could not possess gold, the federal government continued to maintain a stable international gold price until 1968 when it rose to $42.22 before the gold window was closed altogether under President Richard Nixon in 1971. This move led to The Great Inflation of the 1970’s. The limitation on private ownership of gold in the U.S. was repealed in 1974 under President Gerald Ford. In 1977, Congress amended The Federal Reserve Act, stating the monetary policy objectives of the Federal Reserve, its “dual mandate”, as:

"The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy's long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates."

By January 1980, gold had risen to $850 per once. Under Fed Chairman Paul Volcker, the federal funds rate was raised to 20% in June 1980 successfully stabilizing the dollar.

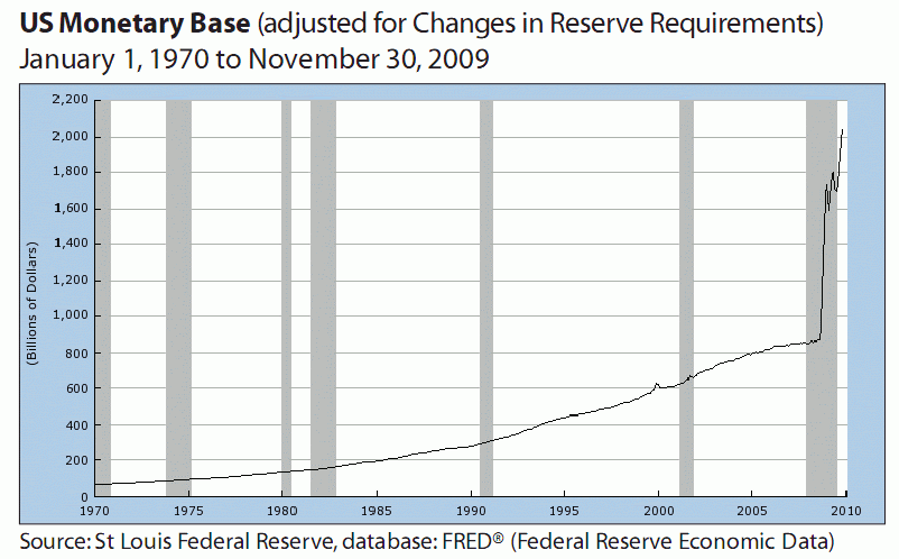

How does the Fed accomplish its “dual mandate”? The Fed sets interest rates by controlling the monetary supply via open market operations (“OMO”),[4] adjusting the discount rate and establishing reserve requirements. The most commonly used tool of the Fed is open market operations. Two examples of OMO are quantitative easing (“QE”) and Operation Twist. In the current rendition of Operation Twist, the Fed affects the yield curve of U.S. Treasury securities by simultaneously selling short-term debt and buying long term via the ostensibly private market of primary dealers. (The Fed’s balance sheet remains unchanged.)[5] The result in this case is artificially low interest rates on long-term U.S. debt, which subsequently brings down the overall market interest for long term debt. QE is the process by which the Fed increases its own balance sheet by creating Federal Reserve Notes (U.S. dollars) to buy financial assets (e.g. U.S. Treasuries and mortgage backed securities, “MBS”) from the market, thereby increasing the monetary base. (This process is often referred to as “printing money”, although technically speaking, the act of physical printing is conducted by the Bureau of Engraving and Printing, a government agency within the United States Department of the Treasury.)

As a matter of fact, this is the primary mechanism by which money is created: the Fed creates U.S. dollars at its own discretion to buy primarily interest bearing U.S. Treasury securities (e.g. T-bills, T-Notes, T-Bonds and TIPS), which, of course, increases the federal debt. In other words, since closing the gold window in 1971, Federal Reserve Notes are effectively backed by nothing more than the government’s promise to pay Federal Reserve Notes. As should be obvious, the result is a circular process in which the U.S. currency has a value supported solely by perception. This perceived value is quite strong, however, as the U.S. dollar remains entrenched as the de facto reserve currency of the world as established by the now extinct Bretton Woods Agreement of 1944, when the dollar was pegged to gold at $35 per ounce.

The monetary base created by the Fed is then multiplied by the process of fractional reserve banking which is also predicated on increasing debt.[6] Currently, depository institutions are required to maintain 10% on deposit with the Fed of all liabilities (i.e. demand deposit accounts) over $58 million. So if a bank is capitalized at $100 million either from deposits or otherwise, it can lend out $90 million; that money is then in turn deposited within the banking system of which 90% can be lent again. This process continues, and the original $100 million money supply of this example approaches $1 billion, asymptotically. The result, by design, is such that as overall debt increases or decreases, so does the supply of money. In other words, instead of the money supply being tied to the total value of goods and services in the economy, it’s tied to the total amount of bank issued debt.

Fractional reserve banking is inherently unstable. If it weren’t, there would be no need for a “lender of last resort”:

“Any exponential, debt-based monetary system is, at its very core, a Ponzi scheme. It simply has to keep expanding so that there’s enough money and credit manufactured today to meet yesterday's principal and interest loads. Without endless growth, sooner or later the debt pile collapses, and truly extraordinary losses are taken by somebody.” [7]

With the financial crisis of 2008 and under the pretense of “too big to fail”, Congress passed the Emergency Economic Stabilization Act establishing the Troubled Asset Relief Program (“TARP”), which authorized the U.S. Treasury to spend up to $700 billion buying distressed assets and supplying cash directly to banks, in addition to allowing the Fed to make interest payments on depository institutions' required and excess reserve balances. Meanwhile, the Fed disseminated over $16 trillion[8] in loans and new currency via QE1 and QE2 over the next two years; the Levy Institute estimates that the Fed committed over $29 trillion increasing its balance sheet from $900 billion to $2.8 trillion.[9] The following table itemizes the recipients of the Fed’s bailout allocations according to the GAO:

In November 2011, the Financial Stability Board formalized the notion that was popularized by U.S. Congressman Stewart McKinney in a 1984, “too big to fail”, publishing a list of global “Systemically Important Financial Institutions” or “SIFIs” including 29 banks in 12 countries:

In response to the lack of improvement in unemployment resulting from QE1, QE2 and ongoing Operation Twist, on September 13, 2012 Fed Chairman Ben Bernanke announced the commencement of QE3 launching an open-ended $40 billion per month MBS bond purchasing program. Bernanke stated that QE3 will continue for a considerable time even after unemployment improves, which lead to QE3’s alternative nickname of QEternity. When asked how buying agency debt will increase employment on proverbial “Main Street”, Bernanke responded:

“We are trying to create more employment, we are trying to meet our maximum employment mandate, so that’s the objective. Our tools involve—I mean, the tools we have involve affecting financial asset prices, and that’s—those are the tools of monetary policy. There are a number of different channels—mortgage rates, I mentioned other interest rates, corporate bond rates, but also the prices of various assets, like, for example, the prices of homes. To the extent that home prices begin to rise, consumers will feel wealthier, they’ll feel more disposed to spend. If house prices are rising, people may be more willing to buy homes because they think that they’ll, you know, make a better return on that purchase. So house prices is one vehicle. Stock prices—many people own stocks directly or indirectly. The issue here is whether or not improving asset prices generally will make people more willing to spend. One of the main concerns that firms have is there is not enough demand, there’s not enough people coming and demanding their products. And if people feel that their financial situation is better because their 401(k) looks better or for whatever reason, their house is worth more, they are more willing to go out and spend, and that’s going to provide the demand that firms need in order to be willing to hire and to invest.”

BENEFITS FROM THE FED [10], [11], [12]

The primary benefit to the Fed’s member banks is not direct profit sharing in the Fed or interest on reserves, but direct access to its low to zero interest money in addition to the “unintended consequences” of its policies such as inflated asset prices and bank consolidations, which coincidentally have tended to favor its biggest shareholders.

"Free money" loans create moral hazard, which means that those who can borrow money for almost nothing and never have to pay it back act entirely differently from those paying market rates for money and backing their loan with real collateral that is at risk. The SIFI banks are simply not incentivized to participate in the real economy in a productive manner. Why would they… they’ve got a centrally managed market of Fed supported returns and risk protection à la the Bernanke Put.

QE does this in two ways – first by dumping money into the banking system, which then has to go somewhere and do something, so some of it ends up in the stock market, and second by driving down interest rates, which reduces the yield on low-risk assets such as U.S. Treasuries and Certificates of Deposit (“CD”) having the tendency to push money into stocks. Why has the Fed pledged this latest round of QEternity? When the stimulus ends, stocks respond unfavorably. It would seem that the Fed is now trapped such that if it ever pulls away from the market there will be a rout of historic proportions, as illustrated in the chart below:

Widely distributed prosperity for the citizenry results from increases in real income that flow from productive investments and higher productivity that's passed on to workers. The Fed's model of "prosperity" is to enrich the banks and incentivize workers to take on more debt to boost their consumption of phantom assets in stock and housing bubbles while continuing to inflate the student loan bubble. For example, banks borrow from the Fed at 0%; students borrow from the banks at 7%. Banks never have to actually pay back their "free money" from the Fed, while students are indentured for life to the banks. The interest on skyrocketing debt drains income and capital from potentially productive investments to pay for unproductive debt-based spending on consumption, friction and mal-investments.

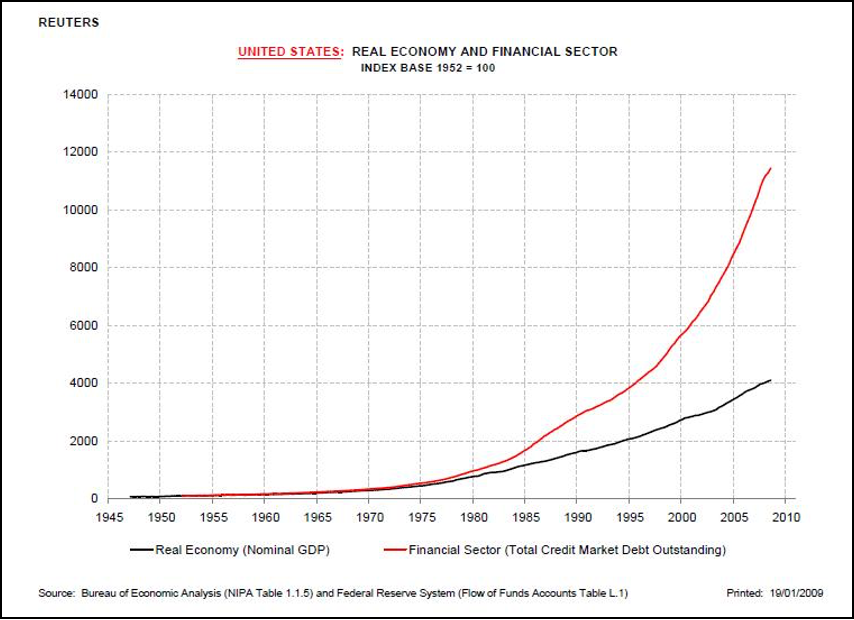

What is the fundamental basis of bank wealth and power? The financialization of the entire economy. And what are the primary mechanisms of financialization? Ever-expanding credit (debt) and leverage based on phantom collateral in phantom assets. And what is the primary purpose of the Fed's policies? To expand debt and leverage. These are the essential mechanisms of increasing the banking sector's wealth, power and control over the economy and the machinery of governance. Expanding debt and leverage is tantamount to expanding banking profits and thus the banks' political power.

The big banks haven’t been the only beneficiaries Fed accommodations, however. Many private funds and foreign companies having questionable economic importance have received funding as well. The following excerpt from a Rolling Stone article “The Real Housewives of Wall Street” published April 12, 2011 highlights one such example:

“…all you have to do is look closely at the taxpayer money handed over to a single company that goes by a seemingly innocuous name: Waterfall TALF Opportunity. At first glance, Waterfall's haul doesn't seem all that huge — just nine loans totaling some $220 million, made through a Fed bailout program. That doesn't seem like a whole lot, considering that Goldman Sachs alone received roughly $800 billion in loans from the Fed. But upon closer inspection, Waterfall TALF Opportunity boasts a couple of interesting names among its chief investors: Christy Mack and Susan Karches.

Christy is the wife of John Mack, the chairman of Morgan Stanley. Susan is the widow of Peter Karches, a close friend of the Macks who served as president of Morgan Stanley's investment-banking division. Neither woman appears to have any serious history in business, apart from a few philanthropic experiences. Yet the Federal Reserve handed them both low-interest loans of nearly a quarter of a billion dollars through a complicated bailout program that virtually guaranteed them millions in risk-free income...”

Any healthy political and financial system would have broken this fraud-based system and dismantled the failed banks en masse in an orderly fashion… potentially going so far as to move from a debt–based currency to an asset-backed one. One institution stopped this from happening: the Federal Reserve. Instead of allowing a failed system to collapse and establish a new one based on prudent lending, market-set interest rates, competitive banks and transparent regulatory structure, the U.S. has a failed system that has become even more politically powerful even as its Fed-backed excesses have increased systemic fragility. In short, the Fed exists to serve the banks and their cronies. Everything else is propaganda.

O CANADA, A SUCCESSFUL ALTERNATIVE TO CENTRAL BANKING

In lieu of fiat currency issued by a central bank, many people advocate for a return to a precious metal standard for currency. While this is likely a better alternative to the debt-based currency system that is currently employed, there are other monetary systems to consider. Canadian history offers a practical example of a successful, elastic alternative to central bank issued debt-based currency. Until the creation of the Bank of Canada in 1935, Canada utilized an asset-backed currency whose stock varied with demand, unlike its U.S. counterpart. Because of dated Civil War legislation (i.e. National Banking Acts of 1863 and 1864) requiring U.S. National Banks to back currency issuance by U.S. Treasury securities, there was little correlation between economic demand for currency and currency issuance. Competing Canadian banks were allowed to issue currency backed by general bank assets… the same assets used to back deposits. The following chart compares the stock of U.S. currency to that of Canada during the late 19th century, a period of rapid economic growth characterized by seasonal harvest periods that required increases in currency supply:

During the Great Depression, Canada did not suffer a single bank failure; the U.S. lost approximately one third of its banks during the same period. (Canada did lose one bank, Home Bank of Canada, in 1923.) Canada’s minimally regulated asset-backed currency system was utilized until populist pro-inflation pressures spearheaded by Major C. H. Douglas led to the creation of Canada’s central bank mirroring the U.S. monetary system.[13]

EFFECTS OF U.S. MONETARY POLICY ON THE GREATER ECONOMY [14], [15]

The whole idea of an economy is to allocate land, labor and capital in a way to maximize productivity and utility of these resources… to increase the standard of living. Capital improves consumers’ productivity, and capital is made available through savings. Like any other price, interest rates represent a price to borrow the economy’s store of savings and are driven by its supply and demand. When there is a lot of savings, interest rates, or the costs of money, go down; when there is less savings, interest rates go up. Ultimately, equilibrium will be achieved creating a market rate of interest.

Money must serve as a store of value to facilitate savings. It’s this savings that finances capital investment and business expansion. This investment enables consumers to generate the productivity required to yield the value to purchase goods and services from others. If consumers weren’t productive, there would be nothing to buy.

Savings also help drive down prices as they are used to increase production in lieu of immediate consumption; lower prices are a benefit of free markets. The Keynesian argument is that if prices fall nobody will buy anything as they wait for prices to fall further. The fallacy of this argument is evidenced in the technology sector by the mass dissemination of computers and cell phones as their prices have fallen over time.

Now that the U.S. has a fiat currency, the Fed is able to and does send false signals to the market when it manipulates interest rates. As a result, investments are made that shouldn’t be made; in other words, resources are misallocated. The booms are caused by this misallocation or mal-investment. For example, to avoid the corrections associated with the bursting of the dot-com bubble, the Fed inflated the housing bubble. When people buy houses, they buy them based on the monthly payment, which is a function of the mortgage rate. When the Fed sets interest rates at 1% leading banks to offer interest only teaser rates on mortgages, it encourages people to become overly vested in real estate as opposed to employing their resources on more productive sectors of the economy. This real estate heavy economy was a function of money being too cheap. Instead of the market setting interest rates, central planners at the Fed picked rates.

When the housing bubble burst, President Bush blamed Wall Street for being drunk. They were drunk… on the liquor provided them by the Fed in the form of excessively low interest rates. A comparison can indeed be made between the tough choices required to allow an economy to correct and a drug rehab facility. When a patient checks in and is suffering from withdrawal, the rehab facility isn’t happy to see the patient suffer, it’s just a necessary aspect of the recovery process. If every time a drug addict checked into rehab, he was given drugs to minimize his suffering, the rehab facility might become a popular destination, but the patient would never be cured. When the narcotic of cheap money begins to wear off and interest rates begin to rise, the painful repercussions of the financial mistakes made during the boom begin to surface. The recession is where the mistakes are corrected; recession is needed to recover a healthy economy. Instead of suffering the full impact of the 2008 financial crisis as was needed for real economic recovery, the Fed has inflated a dollar bubble by disseminating over $16 trillion plus in financial institution bailouts around the world.

In addition to people who made bad investments during the boom losing money, people that have jobs as a result of the boom that shouldn’t exist must lose those jobs so that they can be employed in a different, more productive capacity. Politicians most often don’t differentiate between jobs. They think as long as people have a job, it’s okay… so if one person has a job digging a ditch and someone else has a job filling it in, then they’re both employed, and that is good. It’s not. There’s nothing to show for the labor. Jobs are not an ends; jobs are a means. When people have a job, they want what they can buy with their paychecks, but there’s only something to buy if something is produced. So people have to be employed productively.

Why does the Fed pick such low rates? Politicians like the boom; everybody thinks the boom is good. When voters feel good, incumbents are more likely to get reelected. In addition to the problems caused directly by monetary policy, the Fed supports the politicians further by enabling irresponsible fiscal policy. Policy makers fail to acknowledge that the stimulus is what led to the recession. The minute recession hits, what does the government want to do? Create or expand government programs and benefits that can only be paid for by financing from by the Fed et al. Spending printed money helps the short-term picture and effectively buys votes… people still want their benefits. Everything that needs to be done for the economy is bad politics. These inflated bubbles and inevitable corrections known as the business cycle are exacerbated, if not created, by monetary and fiscal policy.

Meanwhile, the Keynesian perspective suits the politicians’ needs perfectly; Keynesian economists say that there is not enough demand, and it’s a good thing when prices go up, otherwise there would be deflation. They advocate that if Americans are broke more money needs to be printed and the government needs to spend. Spend what? If the people are broke, then the government is broke. The people are broke because they’re loaded up with debt, and they’re not sufficiently productive. Where does the government get its money? Taxes on the production of its people.

This problem was highlighted in the late Soviet Union. The Soviets bragged that they had very low unemployment… everyone worked for the government. Their citizens would have to wait in line six hours for a loaf of bread because no one was baking bread; most of the population was working for the government making a paycheck but in an unproductive capacity. If no one is producing anything then one’s salary doesn’t have any value… it’s just paper. Governments can print money all they want, but they can’t print valuable production.

U.S. fiscal policy is simply designed to postpone the day of reckoning beyond the next election. If giving benefits such as unemployment grows the economy, then why limit it to the unemployed? Why not just give everyone money to scale the projected positive impact on the economy? Such programs don’t grow the economy. Simply look at the debt; it’s grown much more than GDP. The illusion of growth is perpetuated by highlighting only half of the balance sheet. The result is that instead of the government taking the money from its citizens via taxation, it takes the spending power from their money via inflation. So they don’t see the tax, they feel the tax. Financial bubbles such as what’s been experienced in the stock market and housing are one expression of inflation. Another is manifest in increased grocery or energy prices. The government blames those increased prices on greedy oil companies, financial speculation, natural disasters, bad weather, etc. The real price of oil is now less than it was during the 1950’s.

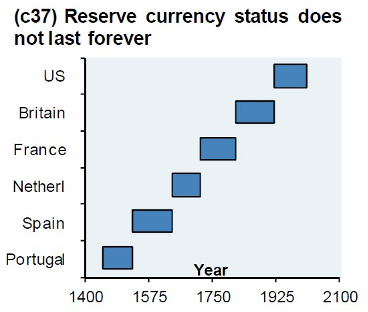

The U.S. government is enabled to perpetuate these problems to an extent greater than any other nation due to the fact that the U.S. dollar remains the world reserve currency. Up until WWII all countries were on the gold standard. After WWII, the U.S. had nearly all the world’s gold. The U.S. got this gold from foreign countries buying the goods it produced. The U.S. became the world’s most productive economy, despite having the world’s highest paid labor force, because it was the world’s freest capitalistic society. U.S. workers were the most productive because of access to capital and limited government regulation. Fueled as the world’s leading economic power, the U.S. proposed a new monetary system where foreign central banks would back their currency by the U.S. dollar, which was of course backed by gold. If foreign banks held dollars, they got interest; if they held gold they had storage costs. This was the crux of the Bretton Woods Agreement. Soon after, the U.S. abused this system by printing more money than it had in gold. Instead of allowing the dollar to correct, the U.S. defaulted by closing the gold window in 1971. The dollar was marked down by about 2/3 during the 1970’s, but it remained the world’s reserve currency. Oil went from $3 a barrel to $30 a barrel; gold went from $35 per ounce to $800 per ounce. As a result of this inflation, the U.S. standard of living declined dramatically and, not so coincidentally, women entered the workforce en masse.

Even though the world marked down the dollar, it stabilized when Fed Chairman Paul Volcker raised interest rates to over 20% in the early 1980’s. Once the world realized the dollar was backed by nothing, however, it became much easier for the U.S. to run deficits… the U.S. no longer had to pretend the dollar was backed by the commensurate amount of gold. This was the beginning of the end of the U.S. being the world’s biggest creditor and producer of high quality, low costs goods. The U.S went through a great transformation from then on as it began to live off the printing press. To cover for its lack of national production, the U.S simply borrows money from the Fed and foreign countries to support endless spending.

When the dollar can be printed out of thin air and the world is going to take it, the U.S. can buy all the products it needs from its trading partners for nothing. The Chinese invest land, labor and capital making things for Americans in exchange for dollars that were simply run off the printing press. And the only thing they can do with them is loan them back to us buying Treasuries (e.g. more dollars). Many people misunderstand this relationship believing that the Chinese benefit from it. The Chinese aren’t gaining nearly as much as the U.S.; the U.S. gets all the stuff, and the Chinese get all the work. The U.S. says that the Chinese get jobs; the slaves had jobs, but that wasn’t a very good deal for them.

The whole idea behind exporting is not to create jobs; it’s to eliminate jobs. The reason a country exports is so that it can import something else; it’s a means to maximize consumption. If there’s something that one country makes better than others, it’s most efficient for that country to focus on making that one thing and trade it for stuff that others make better. Currently, when the U.S. trades with foreign nations, they send the U.S. stuff, and the U.S. says it has nothing for them but an IOU, dollars. Our trade partners, such as China, take the dollars because it’s the world’s reserve currency. They think that one day that they’ll use them to buy something, but the stuff the Chinese want to buy is all made in China.

The U.S. now has this entire bubble of a phony economy that is predicated on Americans borrowing money they didn’t save to buy products they can’t afford and didn’t make. All of the U.S. economic policy is designed to sustain this. As with all bubbles, it can’t last forever and the corrections will occur. The longer the corrections are delayed by centrally planned policy, the bigger the corrections and deeper the recession will be. Interest rates must rise if the economy is going to correct, but that will be extremely painful as the U.S. is so overly indebted. Without market driven interest rates, the U.S. will never have a real recovery.

The bank stress test conducted by the Fed on the 19 largest financial institutions in March 2012 did not include a scenario of an increase in the federal funds rate. Was this because the Fed thinks rates will never go up, or were they concerned about the banks' ability, or inability rather, to remain solvent becoming exposed? The Fed maintains that interest rates will not rise, but it’s impossible that interest rates will never rise. What happens when interest rates do go up? The reason the U.S. is able to pay the interest on its debt is because rates are so low. Banks are going to fail, housing is going to go down more, the government will have to drastically reduce spending, and in fact it may have to default on the bonds it’s already sold. Who’s going to save money (i.e. buy U.S. Treasuries) that’s losing its value at an accelerating rate? Inflation is already substantially higher than what the Bureau of Labor Statistics (“BLS”) reports via its “core” Consumer Pricing Index (“CPI”); the CPI is designed to make inflation appear low as food and energy were removed in 1980. At some point inflation will be so pronounced that the government will be unable to ignore it, and interest rates are going to rise. When interest rates rise, the banks are going to fail again, except this time the government won’t have the ability bail them out. The next time the banks fail, the depositors lose money. If the government can’t cover its own debts, how can it bail out the FDIC? The U.S. is one chapter behind Europe.

When the housing bubble first began to crack in the subprime market, all the experts from the Bush Administration down to Wall Street were on TV reassuring everyone it was contained… it was tiny little problem and the market was sound. The Austrian economists were saying at that time that the problem is not just a subprime problem, it’s a mortgage problem, and it’s not a matter of contagion, everybody is already sick; it’s just a matter of time before the symptoms show up.

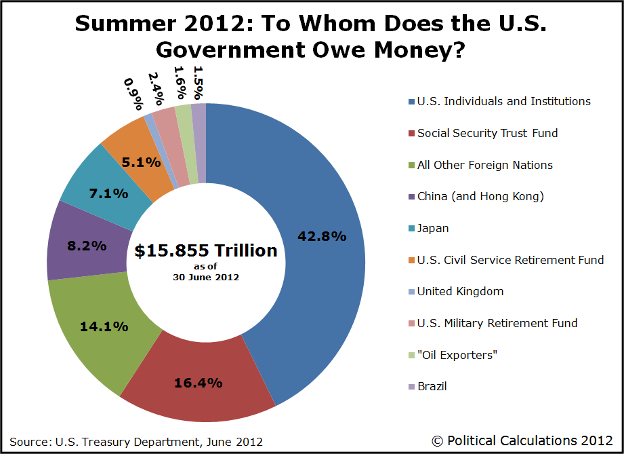

Now it’s the same issue with sovereign debt. This is not an Italian, Greek or Spanish problem; it’s a debt problem, and the U.S has more debt than Europe. The government bubble is the biggest yet, and it is not sustainable. Eventually the Fed will be the only market for American debt as trade partners such as China witness their current holdings deteriorate under inflationary pressures. The real crisis that the U.S. is at great risk of experiencing is a sovereign debt crisis, a collapse of the bond market and collapse of the dollar on a much grander scale than is being seen in Europe. The U.S. having the world’s reserve currency, ability to print money, and support of Keynesian propaganda doesn’t make it immune to the real laws of macroeconomics indefinitely.

Some advocate that simply increasing taxes is the way to fix the problem. The U.S has borrowed more money than its citizens could possibly repay. Raising taxes on the top 1% - 10%, or even the top 99%, can’t even come close to eliminating the debt. It’s going have to come through either a restructuring or default. There are two ways in which this can come to fruition: 1) either Congress can level with its creditors and say it can’t pay 100 cents on the dollar on its outstanding Treasuries and level with people expecting government benefits by means testing to make do with less, or 2) simply inflate the currency into oblivion at which time the dollar will not only not be worth a Continental, it won’t be worth a Federal Reserve Note. The U.S. is not going to be able to continually roll its debt over. Eventually its creditors are going to want to get paid, and the U.S. can’t pay. The U.S. government is not going to do the right thing until there is a crisis. There is a phony crisis every time the Congress is forced to raise the debt ceiling; the U.S. is telling its creditors that it’s running a Ponzi Scheme. The U.S. doesn’t say it will cut spending or raise taxes to cover its obligations; the U.S. says that if it can’t borrow more money, it can’t pay who it already owes. At some point U.S. lenders are going to stop raising the credit ceiling. One way or another the people who have loaned money to the U.S. are going to lose. The longer these mal-investments pile up, the bigger the collapse and harder it will be to restore economic balance. Right now Europe is buying the U.S. time as their situation for the time being is relatively worse.

All these problems result from government and their intervention into free markets mixing capitalism with socialism. Then, of course, the government turns around and blames capitalism proposing that further government intervention is required to solve the problem. The real threat to liberty is that this is such an enormous problem that the U.S. could end up with total government. The solutions are in the market… letting the corrections take place, returning to economic equilibrium, and suffering the short-term consequences.

This chart illustrates the nominal price of the German stock market from 1914 to 1927:

This chart illustrates the real value of the German stock market from 1914 to 1927:

This chart illustrates the real value of the Dow Jones Industrial Average from 1999 to present (adjusted for the value of Gold):

If one assumes ongoing QE will not result in meaningful long-term economic recovery, then long-term “investment markets” ought not to respond positively to it. The securities markets, both fixed income and equities, are, at least in the short term, detached from value fundamentals while being attached to the supply of currency held in the banking system. Making predictions of their future movement is more a game of speculation than that of responsible investing.

One market that is beyond the direct reach of banking conglomerates is that of residential housing rentals. While the residential rental market is affected by the economy at-large, it can be evaluated based upon fundamentals to a much greater extent than the securities markets. Even as manipulated interest rates and speculation have induced artificial housing prices, the rental market has remained relatively stable:

Contrary to what most Realtors and appraisers are likely to proffer, from an investor’s standpoint, it is important to value residential real estate as a function of its rental income as opposed to comparable sales. For an investor, a piece of residential property can and should be viewed analogously to a business. For stocks, the approximate historical average price to earnings (“P/E”) ratio has been 16:1; this concept can be applied to the residential market as a means to determine stable value. A P/E ratio of 16:1 translates in real estate terms to a cap rate (annual net rent divided by value) of 6.25%. As one might imagine, there is stiff competition for “good deals” in residential real estate as many large private funds such as Blackstone Group (BX) have swept in to capitalize on this market.[16] Such competition makes it increasingly difficult to find income generating residential property yielding 6.25% or better, but the advantages of owning real estate purchased at the right price justify the effort.

Outside of real estate, one of the most popular alternatives to the securities markets has been gold. At $1781.00 per ounce, the estimated supply of the world’s gold at 165,000 metric tons[17] is valued at $9,018,526,495,604. While gold and silver have historically been recognized as money, it is not necessary for the world’s supply of gold to reflect the value of the world’s GDP. Gold is simply one commodity amongst many resources that contribute to the world’s total asset value. While the price of gold is likely to continue rising as people hedge against inflationary risk, better value will likely be available in other precious metals, if not other nonfinancial assets altogether. For example, gold currently runs at about 50 times the price of silver; historically; the gold to silver price ratio had been approximately 16:1 until gold began to wildly outrun silver just after the Civil War.

While gold does represent a potentially high degree of safety in terms as capital preservation, it is important to consider the price of other commodities or hard assets when evaluating quality alternatives to stocks and bonds. As with all commodities, there are holding or storage costs to consider that detract from potential appreciation.

To successfully manage any endeavor, one must limit, yet account for the uncontrollable variables while proactively managing the controllable ones. As the public markets are driven primarily by central planning as opposed to economic fundamentals, great opportunity lies within the markets that are furthest removed from the banking system’s fragility, albeit not completely: private markets.

[Update March 21, 2023]

The recent collapse of Silicon Valley and Signature Banks has been one-upped by UBS's rescue of Credit Suisse with a backstop provided courtesy of the Swiss government.

The FDIC can only cover $125 billion of the $18 trillion in exposed deposits across the banking system. Plans are being discussed that would insure all banking deposits, which is an amount that approaches a full year of U.S. GDP.

The banking system is experiencing the greatest unrealized losses since 2008, and the Fed has stated that it will only selectively rescue "systemically important banks"...

Bank crises are followed by restrictive lending and credit, which drives recession, and the Fed looks forced to acquiesce on a return to QE, which will compound inflation.

These inevitable circumstances you’ve just read about have now arrived.

What does all of this mean for you? What can you do to generate substantial growth and real income as the markets experience potentially extreme volatility?

You're invited to speak directly with Ben Summers Thursday at 6 pm EDT alongside other smart accredited investors and financial professionals with a critical eye:

[1] Edwin Vieira Jr., Pieces of Eight: The Monetary Powers and Disabilities of the United States Constitution (2nd ed.), Sheridan Books, 2002

[2] "FAQ - Who owns the Federal Reserve?" Board of Governors of the Federal Reserve System. Retrieved September 14, 2012. (http://www.federalreserve.gov/faqs/about_14986.htm)

[3] Michael D. Reagan, "The Political Structure of the Federal Reserve System," American Political Science Review, Vol. 55 (March 1961), pp. 64-76, as reprinted in Money and Banking: Theory, Analysis, and Policy, p. 153, ed. by S. Mittra (Random House, New York 1970).

[4] "Open Market Operations". New York Federal Reserve Bank. Retrieved October 29, 2011. (http://www.newyorkfed.org/aboutthefed/fedpoint/fed32.html)

[5] “Maturity Extension Program and Reinvestment Policy”. Board of Governors of the Federal Reserve System. Retrieved September 28, 2012. (http://www.federalreserve.gov/monetarypolicy/maturityextensionprogram.htm)

[6] N. Gregory Mankiw, "Chapter 18: Money Supply and Money Demand", Macroeconomics (5th ed.), Worth 2002, pp. 482–489

[7] Chris Martenson, “What to Do When Every Market Is Manipulated,” Peak Prosperity, August 15, 2012, http://www.peakprosperity.com/blog/79470/what-dowhen-every-market-manipulated (accessed September 21, 2012)

[8] United States Government Accountability Office, Federal Reserve System: Opportunities Exist to Strengthen Policies and Processes for Managing Emergency Assistance. GAO-11-696. (Washington DC: U.S. Government Accountability Office, 2011) www.gao.gov/assets/330/321506.pdf

[9] James Felkerson, $29,000,000,000,000: A Detailed Look at the Fed’s Bailout by Funding Facility and Recipient. Working Paper No. 698. (Levy Economics Institute of Bard College, 2011) www.levyinstitute.org/pubs/wp_698.pdf

[10] Much of the content in this section is comprised of material taken directly from the sources cited in footnotes 10 and 11. Quotation marks and indentations were not used to minimize excessive, distractive formatting.

[11] Charles Hugh Smith, “Cui Bono Fed: Who Benefits from the Federal Reserve?” Of Two Minds, September 12, 2012, www.oftwominds.com/blogsept12/cui-bono-Fed9-12.html (accessed September 23, 2012)

[12] Chris Martenson, “The Trouble With Printing Money?” Goldworth Financial, September 18, 2012, www.goldworth.com/artilcedetail.php?id=364 (accessed September 21, 2012)

[13] George Selgin, Bank Deregulation and Monetary Order, (London: Routledge, 1996)

[14] The content in this section represents an edited transcription of the lecture cited in footnote 15. Quotation marks and indentations were not used to minimize excessive, distractive formatting. The three charts comparing the German stock market to the Dow Jones were taken from the article “Zee Stabilitee & The Wealth Effect” published anonymously at ZeroHedge.com on September 15, 2012.

[15] Peter Schiff, “What About Money Causes Economic Crises?” Ron Paul Lecture Series (Washington D.C.), December 19, 2011

[16] Stephen Gandel, “Wall Street’s Hottest Investment Idea: Your House,” CNN Fortune Finance, July 24, 2012, http://finance.fortune.cnn.com/2012/07/24/wall-street-foreclosures/ (accessed July 24, 2012)

[17] "About gold > Demand and supply". Retrieved 10-1-12. (http://www.gold.org/about_gold/story_of_gold/demand_and_supply)